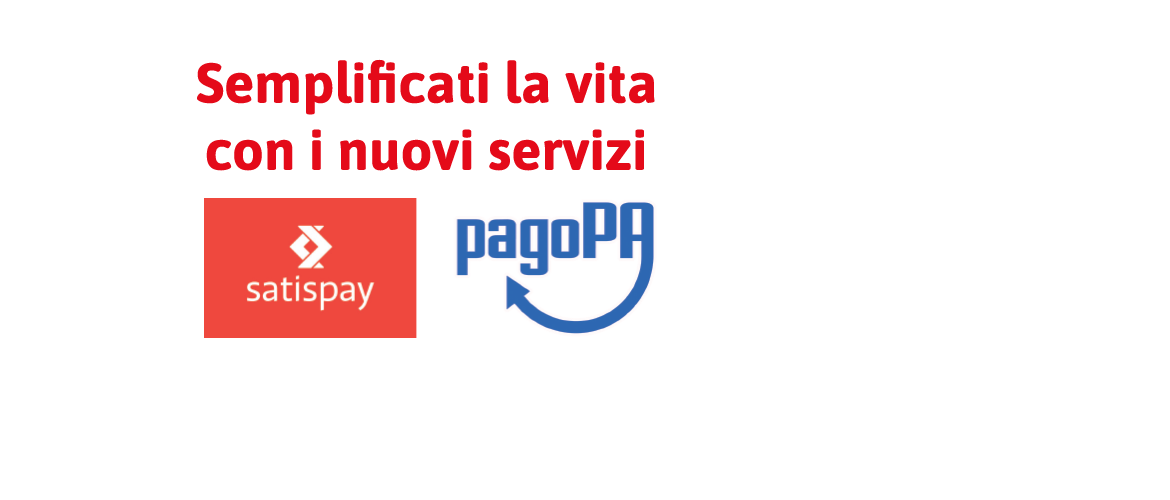

Promozioni

Sfoglia il volantino e tieniti aggiornato su tutte le offerte e le iniziative promozionali

Punti vendita

Cerca il negozio più vicino a te, scopri i suoi servizi e trova la strada per raggiungerlo

Ricette

Tante idee per cucinare piatti semplici e tipici della tradizione italiana

Le Nostre Ricette

Consulta una selezione di consigli per la tua cucina

![]()

![]()

Copyright © 2024 Ipercarni S.r.l. - Tutti i diritti riservati - Sede legale Corso A. Gramsci , 87 - 00045 Genzano di Roma 06 20.99.09.00 Questo indirizzo email è protetto dagli spambots. È necessario abilitare JavaScript per vederlo.

Iscrizione alla CCIAA n° 05604291004 - REA n° 905913. C.F. e P.IVA 05604291004 - Capitale sociale 204.433,00 Int.Vers.

![]()

Copyright © 2024 Ipercarni S.r.l. - Tutti i diritti riservati - Sede legale Corso A. Gramsci , 87 - 00045 Genzano di Roma 06 20.99.09.00 Questo indirizzo email è protetto dagli spambots. È necessario abilitare JavaScript per vederlo.

Iscrizione alla CCIAA n° 05604291004 - REA n° 905913. C.F. e P.IVA 05604291004 - Capitale sociale 204.433,00 Int.Vers.

![]()

Scarica subito la nostra App per iOS su App Store e per Android su Google Play

Scarica subito la nostra App

per iOS su App Store e per Android su Google Play